This week the Justice Department filed yet another suit alleging a financial institution unfairly excluded – or “redlined” — majority-minority neighborhoods from its lending services.

The suit against Minnesota-based KleinBank alleges that between 2010 and 2015, KleinBank conducted its residential mortgage lending in a manner that avoided extending credit to borrowers in neighborhoods where a majority of residents are racial and ethnic minorities.

Followers of the Preiss&Associates blog will recognize many familiar allegations including:

- excluding majority-minority neighborhoods from the bank’s service area;

- failure to place branch offices and mortgage loan officers in majority-minority neighborhoods;

- targeting marketing and advertising exclusively toward residents of majority-white neighborhoods

Kleinbank is fighting back, however.

“We will not admit to wrongdoing when we have done nothing wrong,” said Doug Hile, KleinBank’s president and chief executive officer. “At the end of the day, we’re confident that a fair review of our actual practices and procedures will vindicate us.”

Where KleinBank may have gone wrong

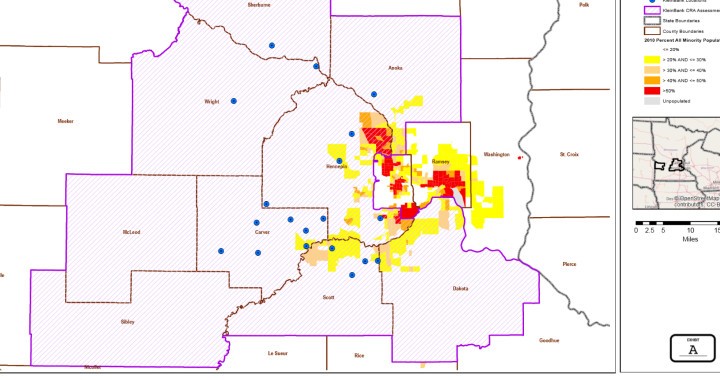

While KleinBank may not have intended to engage in behavior that looked like redlining to the DOJ, a look at their CRA assessment area reveals a weakness that may have landed them on the DOJ’s radar.

According to the Community Reinvestment Act, “…a bank’s assessment area must consist generally of one or more metropolitan areas or contiguous political subdivisions unless that area would be extremely large, of unusual configuration or divided by significant geographic barriers.”

A review of KleinBank’s assessment area (see map above) indicates that the institution did not include one or more metropolitan areas (such as the Minneapolis MSA) or contiguous political subdivisions. Their gerrymandered assessment area excluded an area roughly consistent with the Minneapolis city limits, and using this map for marketing efforts and branch location strategies left the bank vulnerable to redlining claims.

In this era marketing only to your CRA assessment area, even if it is properly drawn, may not be enough. Banks may need to include geographies near their CRA assessment areas when thinking about redlining. For more information on assessment areas, check out our recent blog on “Reasonably Expected Market Areas.” Additionally, banks may want to perform a peer bank analysis to support their choice of assessment area.

Questions?

Do you have questions about how your assessment area may be helping or hurting you?

This year Preiss&Associates celebrates 25 years of providing trusted fair lending and compliance expertise to both large and small institutions. We would be happy to continue that tradition with your institution. Give us a call or send us an email.