In today’s regulatory environment, most compliance officers are keenly aware of the fact that redlining is one of three 2017 foci for the CFPB and probably for the prudential regulators as well. The purpose of this article is to highlight the key elements in any redlining analysis and thereby make it easier for compliance officers either to do their own redlining analysis or to understand the redlining output from a purchased analysis and thereby reduce their redlining risk. The key components of a redlining analysis are: qualitative redlining risk indicators, quantitative redlining risk indicators, peer analysis, mapping and REMA analysis.

Qualitative Redlining Risk Indicators

Qualitative redlining risk indicators of redlining are those indicators that are not numerical in nature. They can often be inferred by reviewing bank applications or lending in disadvantaged geographies such as high minority areas or low and moderate-income geographies. These risk indicators include a bank having a policy of not lending in certain geographies, limiting marketing or soliciting loans only in selected geographies, pricing loans higher in selected areas, offering less advantageous products in high prohibited basis or low/mod geographies and no branches, brokers, LPOs, desk rentals in or near high minority or low and moderate-income areas. Eliminating any or all of these risk indicators is likely to reduce a bank’s redlining risk.

Quantitative Redlining Risk Indicators

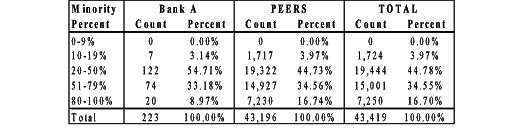

As suggested by the title of this section, these indicators are typically the result of numerical calculations of bank application or origination patterns compared to its peers. These risk indicator comparisons can be done two ways: (1) in percentages and (2) in odds ratios. Of these two alternatives, percentage distributions are most common—that is, a bank’s distribution of loans or originations by race/ethnicity or income class category compared to its peers’ distribution of loans or originations in one of these categories. Table 1 provides an example.

Table 1

In Table 1 Bank A has about 42% (33.18 + 8.97) of its loans in majority minority neighborhoods whereas its peers have a little more than 51% (34.56 + 16.74) in the same majority minority neighborhoods. In terms of the Bank A’s odds ratio, .6917, Bank A is about 31% less likely to have a loan in a majority minority neighborhood. The last question with respect to Table 1 is whether or not the difference between 51% and 42% is statistically important. A statistical test called a t-test (not shown) says the difference is not statistically important. Thus, based on this statistical test, the distribution of Bank A’s loans in majority minority neighborhoods is not very different than its peers. And, the likelihood is that Bank A is not redlining relative to its peers.

Peers

As evidenced by the Peers columns in Table 1 the determination of a bank’s peers can be very important. The regulators often start by choosing a peer set that is all banks in an MSA or those banks that have assets between 50% and 200% of the Target bank (Bank A in our example). They may then, in the spirit of a sensitivity analysis, calculate additional statistics similar to Table 1 but by defining different peer data sets. Typically, these additional peer data sets, often called refined peer data sets by the regulators, are defined such that they more closely match the characteristics of the Target bank. That is, they may match the target bank in terms of loan purpose, loan type, property type, etc. This matching process can be done manually or by using the institutional database matched with the raw HMDA data.

The important part of your peer analysis is that you should do your own peer analysis and not rely on the peer data set the regulators may try to use. After all, who knows your business and who your peers are better: you or your regulator?

One further point about peers. Practice suggests that your final peers list should be the result of a collaboration between compliance and other bank departments. Marketing departments are the obvious candidate to include, but experience shows that they sometimes are myopic and do not include all the reasonable peers. However arrived at, a thoughtful peer listing is important to a bank’s redlining analysis and potentially reduces your redlining risk.

REMAs

REMA is short hand for reasonable expected market area. While the concept of a REMA has been around for some time, it has recently risen to prominence in at least one DOJ matter – Klein Bank. One of the issues in the Klein Bank case is that the institution wanted the analysis done based on its CRA assessment area. According to the regulators a REMA is defined to be where an institution actually marketed and provided credit, or where it could reasonably be expected to have marketed or provided credit. Thus, REMAs do not necessarily coincide with CRA assessment areas. According to the regulators the following factors determine a REMA: (1) where a bank has actually received applications or originated loans, (2) the history of mergers and acquisitions, (3) the market area as defined in bank policies, (4) bank structure and history, (5) advertising and (5) inappropriate exclusion of MMTs from the assessment area. However derived, banks are expected to provide equal access to credit in their REMAs. As in the case of the peers, your input into identifying your institution’s REMAs is very important in possibly reducing indications of redlining.

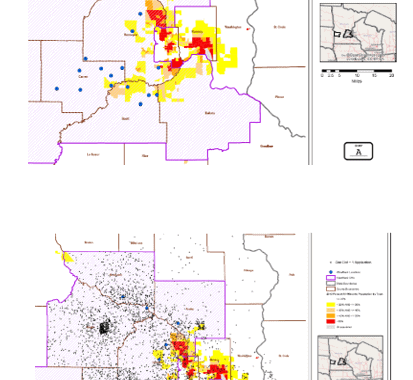

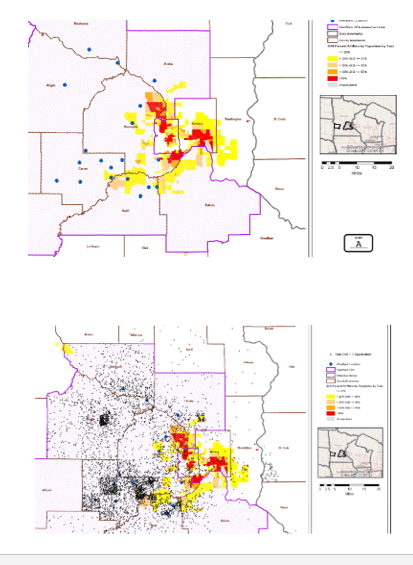

Maps

Mapping is a key to redlining analysis. Using maps, you can identify potential disparate treatment issues, facility location questions, recognize REMAs and look for peers. The maps below are from the Klein Bank case.

Notice in the top map the large dots, which represent branch locations, seem to be mostly outside the colored census tracts. While the branch locations may not prove redlining exists, their locations taken collectively at least warrant a bank explanation. The bottom map, where each dot represents an application, appears to tell the same story. That is, bank applications come from mostly outside higher minority census tracts.

Your Redlining Strategy

Combining these redlining elements and notwithstanding of the size of your institution, your redlining analysis might begin with two separate maps: one for applications and one for originations regardless of whether these applications and originations are in your CRA assessment areas or not. Also include on these maps your branch and other facility locations as well as the high minority and low-mod census tracts. Notice where they might be coverage gaps. The question that then arises is whether or not your competitors are obtaining applications/originations where you are not. A plot of your applications/originations versus the applications and originations of your peers should help answer that question. If there are geographies where your peers are sourcing applications and possibly making loans, then your bank should at least develop a plan to attempt to get a similar share of applications and originations from those geographies.

While not required for smaller institutions, creating tables such as Table 1 for institutions with enough applications or originations shows the statistical analysis referenced in the discussion of Table 1 is appropriate. These statistical analyses can support the bank’s position regarding its current redlining risk and may be used to help explain what the maps show. Furthermore, the maps and the statistics together may serve as a basis for either reducing your existing redlining risk or strategizing what your future redlining reductions tactics may be.

In sum, your redlining analysis is the combination of the several risk factors discussed above. You can reduce your redlining risk by combining these risk factors into a coherent defense of your application and lending patterns for each MSA where you do business